Mortgage Backed Securities Default Rate

Mortgage Backed Securities Held By The Federal Reserve All Maturities Discontinued Mbst Fred St Louis Fed

Mall And Hotel Loans Are Blowing Up Commercial Mortgage Backed Securities Finanz Dk

Which U S Bank Is The Largest Holder Of Mortgage Backed Securities

Residential Mortgage Backed Securities And The To Be Announced Tba Market

Rmbs Issuance In The U S 2019 Statista

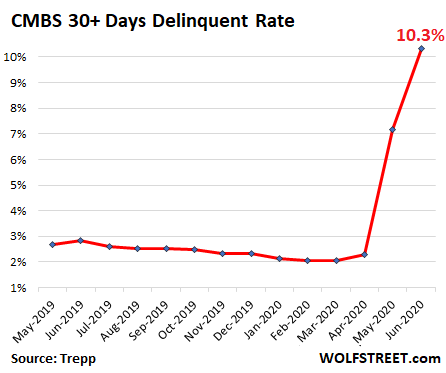

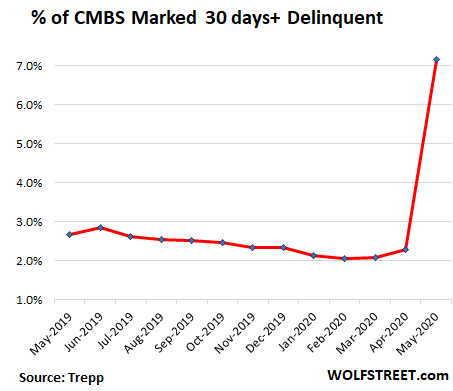

Cmbs Delinquency Rate Spikes By Most On Record Finanz Dk

On the interest rate modeling side there are two primary families of models.

Mortgage backed securities default rate.

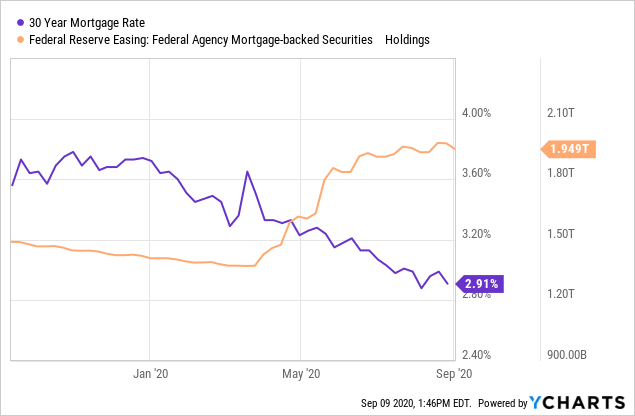

When The Qe Music Stops Us Mbs Will Still Be Dancing Investors Corner

U S Mortgage Delinquency Rate 2000 2018 Statista

Rem 2008 Repeat Risks Growing In U S Mortgage Market Bats Rem Seeking Alpha

Treasury And Agency Securities Mortgage Backed Securities Mbs All Commercial Banks Tmbacbw027nbog Fred St Louis Fed

What Really Caused The Great Recession Institute For Research On Labor And Employment

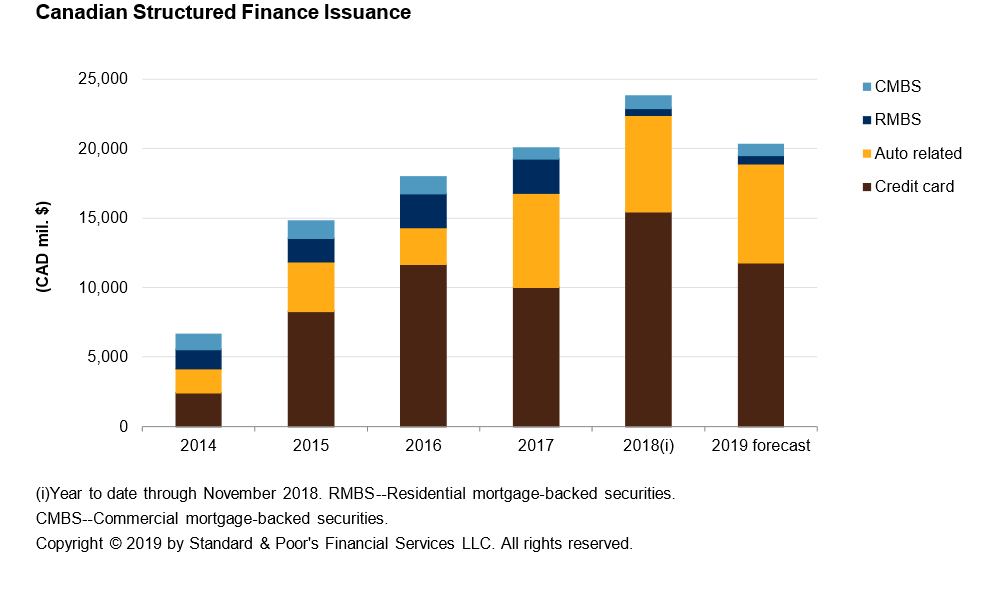

Global Structured Finance 2019 Securitization Energized With 1 T In Volume S P Global

:max_bytes(150000):strip_icc()/dotdash_Final_Why_do_MBS_mortgage-backed_securities_still_exist_if_they_created_so_much_trouble_in_2008_Apr_2020-01-fb17668872fd483781eef521a1ddbde8.jpg)

Why Do Mbs Mortgage Backed Securities Still Exist If They Created So Much Trouble In 2008

4 Gross Issuance Of Non Gse Subprime Mortgage Backed Securities Download Scientific Diagram

New Challenges For Non Agency Rmbs In 2020 Penn Mutual Asset Management

Covid 19 Almost Broke The Bond Market Then The Fed Stepped In

Reverse Mortgage Investment Trust Inc

Https Www Csbs Org Ginnie Mae Issuer Relief Overview And Outlook Pass Through Assistance Program Ptap

Consumer Abs Under Coronavirus In The Us And China Msci

3 Default Rates On Subprime Mortgages Download Scientific Diagram

Source : pinterest.com